In Florida, insurance companies use a 4 point home inspection to check if an older house is still a safe bet. They focus on the roof, electrical system, plumbing, and HVAC. Since our tropical weather is so hard on homes, carriers want to see that these critical systems are in good shape before they agree to cover you.

If you have lived in the Tampa Bay area for a while, you know the “insurance dance.” You get a letter in the mail saying your policy is up for renewal, but there is a catch. They want a 4pt inspection done by a professional. It feels like an extra hoop to jump through, but there is a specific reason for it.

In a state where humidity and storms are constant, insurance companies often require this check-up to make sure your home can handle the next season.

The Reality: Why do they want this report?

Think of a 4-point house inspection like a health physical for your home. Florida homeowners deal with some of the highest insurance rates in the country. To keep those rates from climbing even higher, companies try to avoid “preventable” disasters.

An old water heater that is about to burst or an electrical panel from the 1970s is a ticking time bomb. By asking for a four-point home inspection, the insurance company is looking for a reason to say “yes” to your coverage without taking on a massive risk. It gives everyone peace of mind knowing the home is not hiding a major safety hazard.

What actually happens during the inspection?

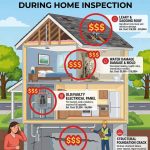

A 4 point home inspection is not meant to be scary. It is a targeted look at the “big four” areas that usually cause the most expensive insurance claims. Unlike a full home inspection that checks every door handle and window screen, this one is strictly business.

Your Roof

The inspector will check the age and the roof covering material. In Florida, the sun bakes shingles until they become brittle. If your roof is over 15 or 20 years old, the carrier wants to know how much life it has left. They are looking for curled edges, missing granules, or any visible signs of a leak.

The Wiring

Old wiring is one of the top causes of house fires. The inspector will open your electrical panel to look for specific brands that are no longer considered safe. They also check for DIY wiring jobs or “double-tapped” breakers where someone tried to cram too many wires into one spot.

The Pipes

Water damage is a nightmare for insurance companies. They will check your system plumbing and HVAC for materials like polybutylene (the gray plastic pipes that were popular in the 80s), which are famous for failing. They also look under every sink for active drips.

Heating and Air

Your heating, ventilation, and air conditioning system must work. Even though we rarely use the heater in Tampa, Florida, law usually requires a permanent heat source to be present. The inspector notes the age and condition of the unit to ensure it is not a fire risk or a mold breeder.

Why do older properties get flagged?

If you own an older property in a place like St. Pete or Clearwater, you are almost guaranteed to need this report. Building codes have changed a lot since the 1990s.

Older homes were often built with materials that we now know don’t hold up as well.

Most 4-point inspections are triggered once a home turns 20 years old, but some companies are now asking for them on homes as young as 10 years. It is simply about the carrier protecting its bottom line against the Florida elements.

Common reasons a home might fail

It can be frustrating to see a home fail a 4-point inspection, but most of the time, the fixes are straightforward. The goal is to catch the “red flags” before they turn into a flooded living room or a fire.

Common “deal-breakers” include:

- Fuses instead of breakers: Most modern insurers want to see an updated panel.

- Leaking water heaters: If there is rust at the bottom, it is a sign of trouble.

- Granule loss on the roof: This shows the roof is no longer shedding water correctly.

- No central heat: Window units usually do not count as a permanent heating system.

If the report shows a problem, you usually have time to fix it. Once you show the insurance carrier that the repair is done, your coverage is typically good to go.

FAQs

How is this different from a regular inspection?

A full home inspection is for you, the buyer. It covers everything from the appliances to the fence. A 4 point house inspection is for the insurance company. They only care about the four systems that could cause a massive claim.

How long will the inspector be at my house?

Because the inspection cover area is limited, it usually takes about 45 minutes. The inspector needs to see your water heater, the AC unit, the electrical panel, and the roof.

Can I use an old report?

Probably not. Most insurance companies require a 4-point inspection to be less than 12 months old. If you are switching companies, they almost always want a fresh look at the property.

Do I need this for a condo?

It depends on the building. Often, the association handles the roof, but the insurance company might still want to see the plumbing and electrical inside your specific unit.

Get Your Insurance Paperwork Ready

Dealing with Florida insurance can be a headache, but your inspection should not be. Robbins Home Inspections knows exactly what local agents and carriers are looking for. We provide clear, photo-filled reports that help you get your coverage quickly.

Get Your Free Quote Today!